Currently, there are just a few insurance companies that offer SAM insurance in the U.S. Oftentimes, the coverage can be expensive and only provide smaller limits, such as up to $1M each occurrence / $1M annual aggregate. Due to the large number of SAM claims, your readiness to pay for SAM insurance is not enough. You must also qualify by having tools and controls in place (e.g., no one-on-one policy, no closed-door policy, background checks, a written and formal SAM incident reporting and investigation policy, and more).

What you may not know is that some insurance companies also require that you, as the insured, be directly involved in the SAM incident; they will not cover any SAM allegations involving “third party on third party.”

Here is a brief review of these limitations and how to approach them.

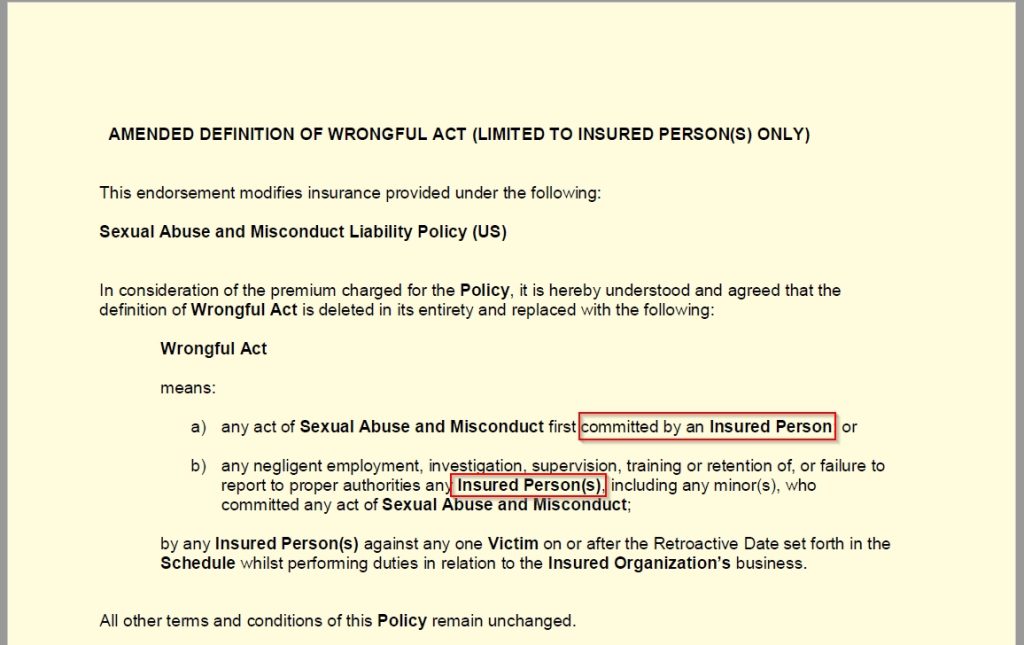

DEFINITION OF WRONGFUL ACT (LIMITED TO INSURED PERSON(S) ONLY)

- If your afterschool instructor walks out and the kids are left alone, and something happens between the children during that time, the policy will not respond.

- Or if a parent or visitor harms a child during your program.

- A school employee (not employed by you) harms a child during your program. Not covered. That employee is not your insured person.

Any natural person who was, is, or during the Period of Insurance becomes: a) a director, officer, or trustee of the Insured Organization; b) a Manager of the Insured Organization, including all persons outside the United States serving in a functionally equivalent role for the Insured Organization; c) an Employee; or d) an Independent Contractor, but only to the extent they are acting for and on behalf of the Insured Organization in such capacity. Insured Person also includes the lawful spouse, civil or domestic partner of any natural person specified above in the event of such natural person’s death, incapacity, or bankruptcy (with some limitations).

So, this endorsement turns such a policy into coverage only for misconduct by your own staff or your organization’s negligence related to your own staff. Anything involving third parties or child-on-child situations is excluded. However, some carriers will not limit their coverage as shown above. If you are looking for SAM Insurance for a special event or a full annual policy, contact us and we will be happy to provide you with an option that fits you best.