[two_third]

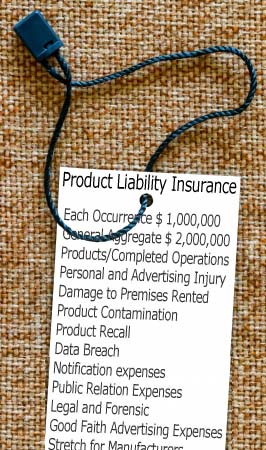

Product Liability Insurance

Covers liability incurred by a manufacturer, importer, wholesaler, retailer or distributor because of injury or property damage resulting from the use of their product. Although, coverage may be provided worldwide, the claim has to be brought into the United States.[/two_third]

[one_third_last]

[button align=”center” link=”https://www.paperless-insurance.com/line-of-business/product-liability-insurance/product-liability-insurance-sample-quote/” color=”green”]View Sample Quote[/button]

[button align=”center” link=”https://www.paperless-insurance.com/line-of-business/product-liability-insurance/product-liability-insurance-quote/” color=”yellow”]Get a Quote Now[/button]

[/one_third_last]

Product Liability Insurance Coverage Highlights

In general, a Product Liability Insurance policy may include the following coverage provisions:

In general, a Product Liability Insurance policy may include the following coverage provisions:

[list icon=”check” color=”green”]

- Bodily Injury – Physical injury to the person of a Third Party. This includes sickness, disease, pain and suffering, emotional distress, loss of income and even death.

- Property Damage – Damage or destruction including loss of use of a Third Party’s property. Reduction in value is the measure of Property Damage.

- Medical Payments – This coverage reimburses the insured and others up to a certain limit for medical or funeral expenses as a result of bodily injury or death by accident

- Fire Legal Liability – Limited coverage for damage to a premise caused by a fire for which you may be held liable.

- Personal/Advertising Injury – Covers you for certain offenses you or your employees commit in the course of your business, such as libel, slander, disparagement. Usually excludes any and all copyright or trademark infringement.

[/list]

How Product Liability Insurance Works

Under a product liability insurance policy, the insurer is obligated to pay the legal costs of a business in a covered product liability claim or lawsuit. Covered liability claims include bodily injury, property damage, personal injury, and advertising injury (damage from slander or false advertising). The insurance company also covers compensatory and general damages. Punitive damages aren’t covered under product liability insurance policies because they’re considered to be punishment for intentional acts. Product liability insurance policies always state a maximum amount that the insurer will pay during the policy period. Usually, these policies also list the maximum amount the insurer will pay per occurrence. For example, if a company has a $2 million each occurrence limit in its liability policy and it’s successfully sued for $2.5 million, the insurer would pay $2 million and the business would be responsible for paying $500,000.

All businesses can take certain steps to lower the chance of a liability insurance claim:

[list icon=”exclamation” color=”green”]

- Set a high standard for product quality control;

- Make sure all company records are up-to-date;

- Train employees properly;

- Get safety tips for your business from the insurance company.

[/list]

Why Product Liability Insurance?

In product liability insurance terms, a product is any physical item that is sold or given away. Products must be “fit for purpose”. Under the Article 2 of Uniform Commercial Code § 2-314 and Tort Law, you’re legally responsible for any damage or injury that a product you supply may cause. If you supply a faulty product, claimants may try to claim from you first, even if you did not manufacture it. You’ll be liable for compensation claims if:

[list icon=”arrow” color=”green”]

- your business’ name is on the product – i.e. the manufacturer made it for your brand

- your business repairs refurbish or change the product

- you imported it from outside the United States

- you cannot clearly identify the manufacturer

- the manufacturer has gone out of business

[/list]

Otherwise, the manufacturer is liable – or the processor, where the product involves parts from multiple manufacturers. However, you must also:

[list icon=”arrow” color=”green”]

- show that the products were faulty when supplied to you;

- show that you gave consumers adequate safety instructions and warnings about misuse;

- show that you included terms for return of faulty goods to the manufacturer or processor in any sales contract you issued to the consumer;

- make sure that your supply contract with the manufacturer or processor covers product safety, quality control, and product returns;

- have good quality control and record-keeping systems.

[/list]

Who needs to carry Product Liability Insurance

Although the ultimate responsibility for injury or damage in products liability cases most frequently rests with the manufacturer, liability may also be imposed upon a retailer, wholesaler, middleman, bailor, lessor, and other party wholly outside the manufacturing and distributing process.

In many cases, you are not be at fault of selling a defective product; however when the claim is brought you need to defend yourself in court. Nowadays, litigation costs are extremely high, so paying it out of your own pocket might affect your business dramatically. Here when product liability insurance comes to play. It will pay for the defense cost up to the amount specified in the policy, your business is not affected financially, and you can continue your growth.

What if the products I sell are manufactured overseas

Imagine how many Chinese manufacturers are actually subject to process from a United States court today and how likely is it that a claimant can enforce a judgment against them? The answer is none and not likely.

This puts a very real risk of liability upon the supplier – the local toy store, convenience store, wholesale supplier, distributor, et cetera. Product liability insurance covers against this kind of risk.

What is The Surplus Line Association?

A nonprofit 501(c)(6) organization, the Association has been working with your state Department of Insurance CDI) to maintain a responsive and lawful State surplus line market. The Association performs statutory duties within your state insurance industry under the direction and supervision of the CDI.

How Much does Product Liability Insurance Cost

The premium generally starts at $350 (selected U.S. States only) per year for small businesses with some low-risk products, like manufacturing of paper, plastic, metal products, computer components, water, and so on. It goes up with the size of the company and higher risk products. Please see our Recent Deals information to get an idea on how much product liability insurance can cost.

What is Product Recall Insurance

Insurance coverage for the cost of getting a defective product back under the control of the manufacturer or merchandiser that would be responsible for possible bodily injury or property damage from its continued use or existence. Standard product liability insurance does not cover this exposure.

How to Protect my Business

You can protect yourself in several ways:

[list icon=”arrow-circle” color=”green”]

- Secure a product liability insurance policy.

- If you do not manufacture the products you sell you need to collect the certificate of insurance from the actual manufacture where you are named as an additional insured. This can help to lower the amount of money your product liability insurance company will pay out on your behalf.

- Test the product to catch when the products were faulty when supplied to you.

- Give consumers adequate safety instructions and warnings about misuse

- Included terms for return of faulty goods to the manufacturer or processor in any sales contract you issued to the consumer.

- Retailers, wholesales, distributors, and importers have to make sure that your supply contract with the manufacturer or processor covers product safety, quality control and product returns.Have good quality control and record-keeping systems.

- Be prepared for product recall. When possible document all sales, shipments, complaints. Be product recall ready.

[/list]

Admitted vs. Non-Admitted Insurance Company

Non-Admitted Means – Insurance carriers not licensed by your State (also called “surplus line carriers”)

[list icon=”arrow” color=”green”]

- Carriers on the List of Approved Surplus Line Insurers (LASLI) (are actually “admitted” insurance carriers, licensed in a state or country of domicile other than your State);

- Carriers that must meet strict surplus line laws and regulations in order to provide insurance to your State businesses and residents;

- Carriers regulated by their state or country of domicile, including stringent requirements regarding reputation and integrity, capitalization and solvency, licensing and business practices.

[/list]

Surplus line insurance policies are sold by “non-admitted” carriers through licensed “surplus line brokers.” Other insurance agents and brokers must go to a licensed surplus line brokerage to access non-admitted carriers. When such companies are on List of Eligible Surplus Line Insurers they are regulated.

Non-Admitted Or Surplus Line – Non-admitted does not mean non-regulated.

Non-admitted carriers on the LASLI have been reviewed and approved by the State Department of Insurance for surplus line insurance in your state. Non-admitted carriers on the LASLI are actually “admitted” insurance carriers in their state or country of domicile other than your state. Surplus lines have been written by non-admitted carriers since the 1800’s, and generally are used when a risk is unusual, unusually large or when coverage is not available from carriers licensed in your state.

Solvency Regulations – Non-admitted insurers on the LASLI must demonstrate

to the your State their financial stability, reputation and integrity; maintain a minimum of $15 million in capital and surplus at all times (for the State of California, please refer to your state requirements); have 3 years seasoning (or qualify for an exception); have a valid license to transact insurance in their domicile; file financial information with the Department of Insurance and adhere to specific capitalization, investment and solvency standards established under the your state Insurance Code.

State Law

– Your State Department of Insurance (DI) is the official regulatory agency for insurance in your state, including the surplus line industry. The Surplus Line Association of your state is officially a nonprofit advisory organization, which performs statutory duties for the DI. The Association’s recommendations are considered and incorporated into the legally binding decisions of the DI when appropriate.